Examining AI-fueled volatility

Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways

- AI disruption has cascaded across multiple industries, driving notable dispersion

- History has shown that technological revolutions have been profoundly positive

- The indiscriminate selling is likely an overreaction to the AI disruption threat

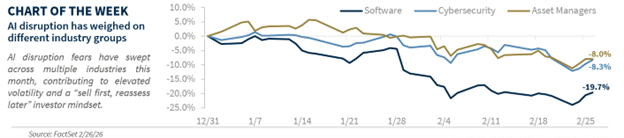

AI-related disruption has moved to the forefront of market conversations in recent weeks, driving shifts beneath the surface. While the S&P 500 remains near all-time highs, leadership has rotated across sectors as concerns about AI’s impact on future demand and long-term valuations have spread, contributing to elevated volatility and a ‘sell first, reassess later’ mindset.

Importantly, these moves have not been driven by weakening fundamentals. The economy remains resilient, and 4Q25 earnings were solid. Instead, sentiment shifted following the release of new AI tools from emerging startups, intensifying fears of disruption and pressuring industries seen as most exposed.

Below, we outline how to interpret the recent price action, explain why we believe the market’s reaction may have been overstated, and discuss what AI’s continued evolution could mean for the economy and financial markets in the months ahead.

AI disruption impact on the economy

Artificial intelligence’s transformational impact on the economy is still unfolding. Given the rapid pace of change, and tepid job growth recently, it is understandable that concerns about AI’s effects on growth and employment have intensified. Forecasts range widely, from substantial productivity gains to widespread job destruction.

However, history offers valuable perspective. Past technological revolutions, including electricity, the automobile, computers and the internet, did not reshape the economy overnight. The benefits emerged only gradually as businesses redesigned processes, retrained workers, restructured how work was done and developed entirely new products. While each wave brought periods of disruption, the long-term impact was profoundly positive: higher productivity, stronger economic growth and a healthier labor market.

AI disruption fears trigger sharp sector rotations

The latest bout of volatility has led to an intense sell-off across several industries of the S&P 500 whose business models are perceived as vulnerable to AI disruption.

Software: The release of new AI tools, including those targeting the legal space, has sparked concern about future software demand. Combined with already elevated valuations, these fears led to a sharp sell-off in the software sector, now down >25% from recent highs.

The software industry has historically been defined by two core attributes: steady cash flows and strong growth, factors that have supported premium valuations versus the broader market. While some worry that new AI tools could displace software products, a more realistic scenario is that AI becomes embedded across software platforms, enhancing productivity rather than replacing current offerings.

This was highlighted at Anthropic’s Enterprise Agent event this week, where Anthropic unveiled partnerships with a broad range of applications from tax (Intuit) to clinical trials (Novo Nordisk) to customer engagement (Salesforce). With software valuations sitting at their lowest level since 2018, and forward earnings still resilient, we view the recent pullback as an attractive opportunity. That said, we would lean toward established leaders, with domain expertise and deep integration into customers’ workflows.

Cybersecurity: Anthropic released a new tool, Claude Code Security, which scans code and databases for vulnerabilities and provides targeted developer recommendations. The launch led to a sharp sell-off across cyber names, with many falling ~10% on the news.

Cybersecurity is a critical pillar in the AI buildout. As data becomes more deeply embedded in business processes and AI-driven attacks intensify, demand for security solutions should accelerate. With global cybercrime costs projected to exceed $15 trillion by 2030, up from ~$10 trillion last year, the need for robust protection continues to grow.

In response, hyperscalers and semiconductor companies are increasingly incorporating cybersecurity into their platform ecosystems to safeguard against rising risks. With cybersecurity now an essential line item in enterprise budgets, demand should remain resilient. While headline-driven volatility may persist in the near term, we remain constructive on the industry’s long-term outlook given the durable, structural demand for cyber protection.

Wealth managers: The launch of a new AI tool from the tech start-up Altruist, which generates customized investment and tax strategies for individuals, sparked a sell-off in financial advisory stocks, sending many names down nearly 10% on the news.

We’ve seen this playbook before. More than a decade ago, when robo-advisors first emerged, there were widespread fears that they would replace traditional financial advisors. Yet despite the concerns, that outcome never materialized. Instead, robo-advisors became just one component of the broader wealth-management ecosystem, not a substitute for relationship-based advice or the value proposition for an advisor.

Clients prefer personal relationships and the reassurance of a trusted advisor, especially when markets get challenging. While today’s AI tools have more capabilities, the outcome is likely the same: new technologies will not replace advisors, but can help them deliver more efficient, personalized, and better outcomes for their clients, suggesting the recent sell-off was overdone.

Bottom Line

AI fears have fueled outsized volatility in recent weeks as markets attempt to separate potential beneficiaries from those more likely to be challenged. That said, we believe the indiscriminate selling cascading across different industries has been excessive.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.